Term vs. Whole Life Insurance: Which Policy Fits Millennials in 2025? - BERITAJA

.jpg)

Introduction: What Challenge Do Millennials Face in 2025?

M

illennials—people born between 1981 and 1996—are now between 29 and 44 years old in 2025. Many are raising families, buying homes, and building wealth. Life insurance, once viewed as a product for older generations, has become central to their financial planning.

According to a 2024 LIMRA (Life Insurance Marketing and Research Association) survey, 46% of millennials in the United States reported needing life insurance, yet only 32% owned a policy. This gap highlights confusion about which product—term life or whole life insurance—best fits their lifestyle and budget.

Photo by Elin Melaas on Unsplash

Why Is This Topic Important?

Life insurance provides financial protection. In 2025, economic uncertainty, student loan debt, and inflationary pressures make it essential for millennials to secure cost-effective coverage.

A 2023 Federal Reserve report noted that the average American household carried $59,580 in debt. Millennials, balancing debt repayment with saving for retirement, must evaluate policies carefully.

Thus, the debate—term life vs. whole life—isn’t academic. It directly affects financial security for millions of U.S. households.

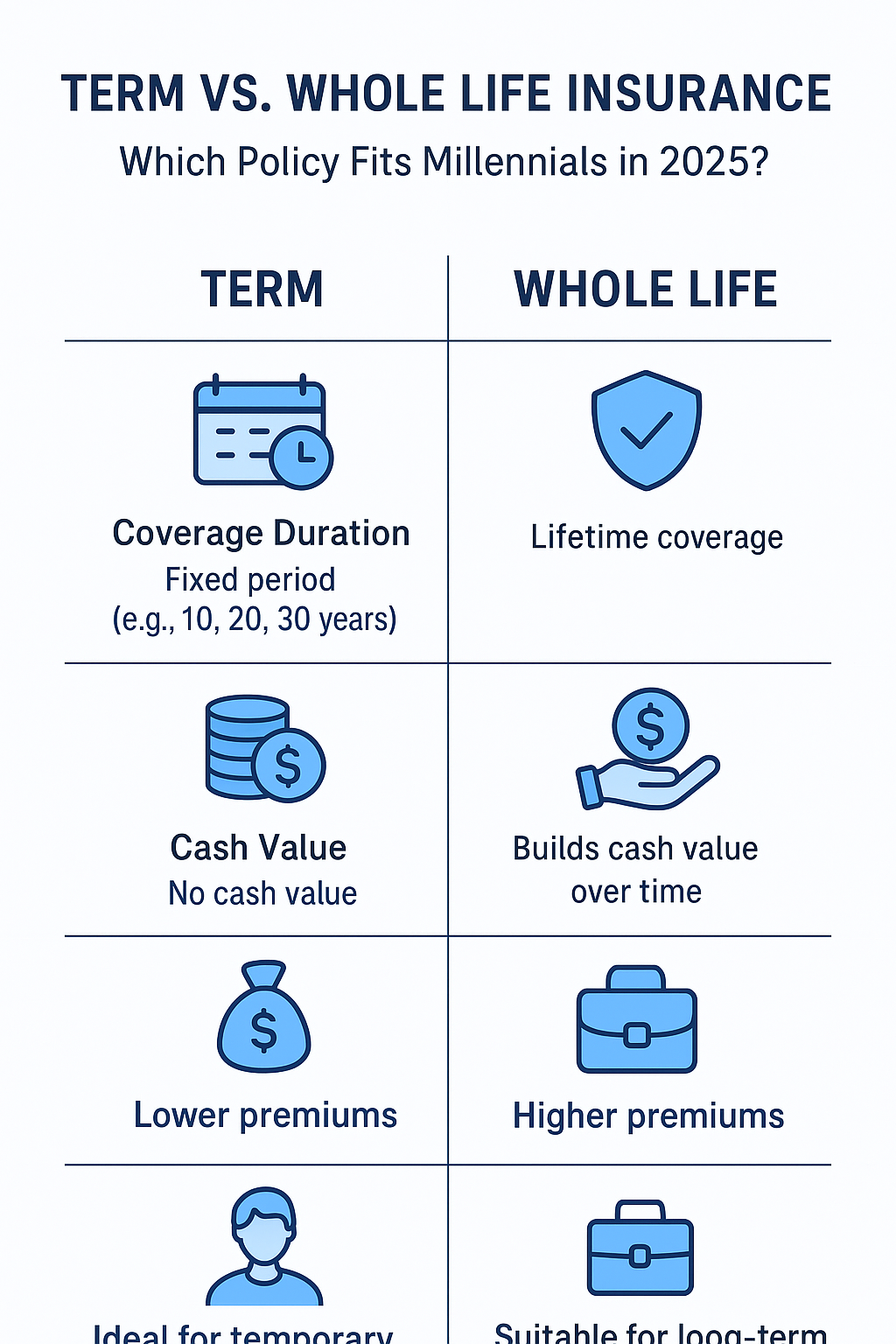

Step-by-Step Breakdown: Term vs. Whole Life Insurance

What Is Term Life Insurance?

- Coverage lasts for a fixed period (10, 20, or 30 years).

- Premiums are lower compared to whole life.

- Policies are straightforward—if the insured dies during the term, the beneficiary receives a payout.

- Example: Prudential Financial offered a 20-year term policy in January 2025 for $28/month with $500,000 coverage (average for a healthy 30-year-old non-smoker male).

What Is Whole Life Insurance?

- Provides lifelong coverage.

- Builds cash value that grows tax-deferred.

- Premiums are significantly higher—typically 5–10x more than term.

- Example: New York Life Insurance Company in a 2025 policy quote: $250/month for $500,000 coverage with cash accumulation benefits.

Cost Comparison Table (2025 Averages)

| Provider | Term Life (20 years, $500k) | Whole Life ($500k) |

| Prudential | $28/month | $240/month |

| MetLife | $30/month | $255/month |

| New York Life | $32/month | $250/month |

TIMELINE

Suitability for Millennials

- Term life: Ideal for those with temporary obligations like mortgages, children’s education, or debt payoff.

- Whole life: Better for millennials focused on wealth transfer, long-term estate planning, or building an investment-like safety net.

Case Study: A Millennial Family in 2025

Meet Jessica Martinez, a 34-year-old software engineer living in Austin, Texas, with her husband and 2 children. In March 2025, she evaluated policies from Policygenius, Prudential, and MetLife.

- Jessica chose a 20-year $500,000 term life plan for $29/month.

- Her reasoning: she plans to be debt-free by 2045, when her children finish college.

This illustrates how financial goals, not just cost, drive the decision.

Academic & Industry Research Insights

- Harvard Business School (2024) reported that 71% of millennials prefer flexible insurance products with digital policy management.

- National Association of Insurance Commissioners (NAIC) in October 2024 found that whole life policies represented 35% of new policies sold, while term life held 65% share, showing millennials lean toward affordability.

- Forbes Advisor (January 2025) noted Prudential, MetLife, and New York Life as consistently top-ranking U.S. providers based on claims settlement ratios and customer satisfaction.

Tips for Millennials in 2025

- Start Early – Buying life insurance at 30 vs. 40 reduces premiums by up to 40%.

- Use Online Quote Tools – Platforms like Policygenius and NerdWallet allow comparison within minutes.

- Assess Financial Goals – If you need protection for dependents only, term life is enough. If you aim to build wealth, whole life works better.

- Check Insurer Stability – Always verify ratings from AM Best or Moody’s.

- Blend Strategies – Some millennials buy term life plus invest separately in ETFs or retirement accounts instead of whole life.

Conclusion: Which Policy Fits Millennials in 2025?

The decision between term and whole life insurance is not one-size-fits-all.

- Term life fits most millennials in 2025 who want affordable coverage during their prime earning years.

- Whole life appeals to those seeking permanent protection and wealth transfer tools.

As of 2025, most millennials benefit from starting with term life and revisiting whole life later, once debt is lower and disposable income higher.

FAQs

Q1: Is term life cheaper than whole life in 2025?

Yes. Term life averages $28–$32/month, while whole life is $240–$255/month for $500,000 coverage.

Q2: Can millennials switch from term to whole life later?

Yes. Many providers, including Prudential and MetLife, allow conversion without a new medical exam.

Q3: What percentage of millennials own life insurance in 2025?

According to LIMRA (2024 data), only 32% of millennials have coverage.

Q4: Which companies rank best for millennials?

Prudential, MetLife, and New York Life consistently rank among the best life insurance companies in the U.S.

")